For the first time, an extensive German review has analysed the costs of sterile goods in hospital, considering all factors from personnel to material. [1] The authors hope that their findings will support hospital managers deciding on sterile goods options. The following text is a summary of the German paper.

Economically challenging times mean hard choices

In light of ever-decreasing healthcare budgets, hospitals across the globe need to be efficient and financially sustainable. There are probably very few, if any, institutions whose managers are not required to assess and monitor the financial impact of all components used in patient care.

As the authors point out, clinical pathways are a crucial instrument for any economic assessment. These pathways include, in detail, all processes that are necessary in the treatment of a patient, from admission to discharge, and are a proven instrument to monitor and increase cost-effectiveness of health care.

One process within these pathways that is frequently neglected by hospital managers is the process of reusable devices and their packaging in a hospital’s “Central Sterilisation Supply Department” (CSSD), warn the researchers. From a clinical point of view, the sterilisation process is of course of the utmost importance for the quality of care in a hospital, especially in surgery. Reusable devices have been shown to be a significant contributor to the costs of the entire treatment process. It is therefore perhaps surprising that currently, only very little is known about the costs associated with these CSSD processes.

Packaging options: how do they differ?

How do packaging options come into it? Sterilised goods including surgical instruments need to maintain their sterility until they are used in surgery or otherwise, and a professional packaging system is crucial in this respect. Currently, there are two main systems on how to wrap a standard surgical instrument set:

- A “non-woven sterilisation wrap” is a one-way material covering the sterilised instrument set; once used, the wrap is disposed of. These wraps are available in a wide variety of different types and qualities. They are further classified as either;

i) Sequential wraps, made of two sheets of wrap per set, one wrapped after the other, or

ii) One-step wraps, made of two layers of wrap thermally sealed along the sides. - “Sterilisation containers” are made for frequent re-use and can be used over a wide range of set weights.

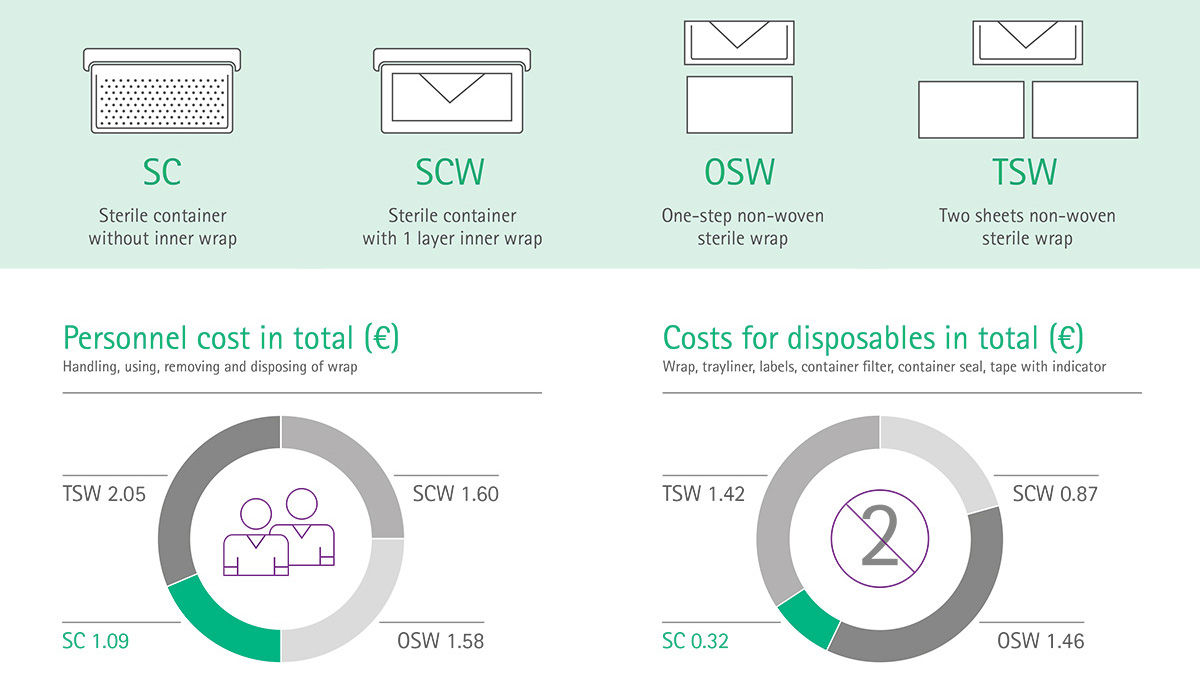

Both wrapping and container packaging can be combined in various alternatives. The present study focused on four different options:

- Sterilisation container with inner wrap (SCW): The sterilisation set is wrapped with a single layer and placed in a container (the wrap material used is typically of lower quality).

- Sterilisation container without inner wrap (SC): As sterile containers are rigid, sterile barriers systems, inner wrapping is not obligatory. Most hospitals worldwide use this form of containing surgical instruments.

- Two sheets non-woven sterilisation wrap (TSW): The traditional way of wrapping sterilised sets first in one, then in another sheet of wrap, whereby the two wrapping processes are separated.

- One-step non-woven sterilisation wrap (OSW): the set is wrapped with a one-step wrap (as explained above, these wraps are made of two layers thermally sealed along the sides).

All four options are widely used in Europe and North America, and, according to the authors, all have shown different advantages and disadvantages, such as containers needing to be cleaned, disinfected and reprocessed and needing more space; wraps leading to a high volume of waste. Most importantly though, the vast majority of manufacturers of all four varieties are compliant with DIN EN ISO 11607 requirements, which means that sterility (up to point of use) and therefore the main marker of quality is usually ensured for all options. For the purpose of the present study, it was assumed that all four options are equal in quality.

What has been missing until now is a detailed cost analysis comparing these four options, making it difficult for hospital managers to choose. In the present paper, the authors analyse the processes and resource consumption associated with each of the four different packaging options and provide recommendations for hospital managers.

What were the detailed steps of the analysis?

The authors chose two German CSSDs as sources for process information: one department that mainly uses non-woven sterilisation wrap, and one that predominantly uses sterilisation containers. Next, the main processes and sub-processes of the sterile supply cycle were defined to determine as accurately as possible which steps require how much time of how many personnel (the authors actually used stopwatches during the observation period). To give some examples, sub-processes include “preparing the container”, “disposing of inner wrap” or “covering tray with first wrap layer, adding label”. This diligent method allowed the authors to determine the “total process time” of all sub-processes, that is to say, the minimum overall time which one single instrument tray needs to go through from CSSD to the operating room (OR).

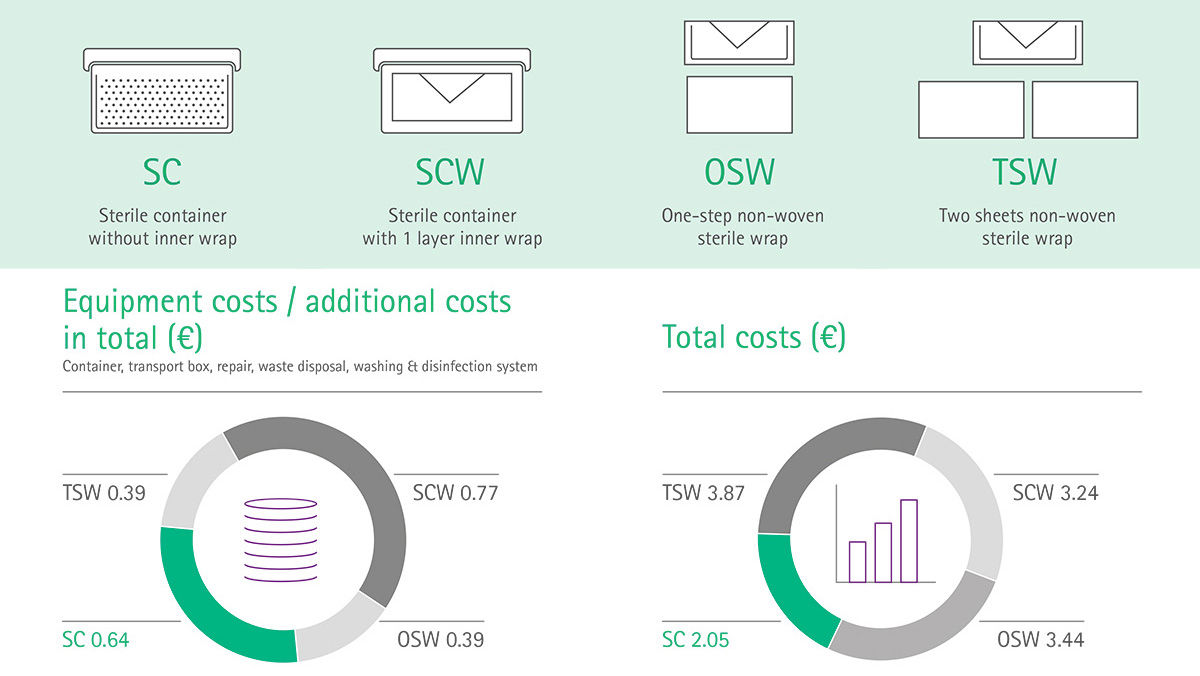

The next step was the cost analysis. This included three main categories:

- Personnel costs: e.g. working days, employer salary per year

- Variable costs: e.g. wraps, tray liners, labels, container filter and seals, tapes

- Fixed and jump-fixed costs: e.g. containers, waste disposal, water and power for washing systems and chemicals.

(Variable costs vary with output, jump-fixed costs are the same fixed costs until a certain number of units is used, then jump to a new fixed cost).

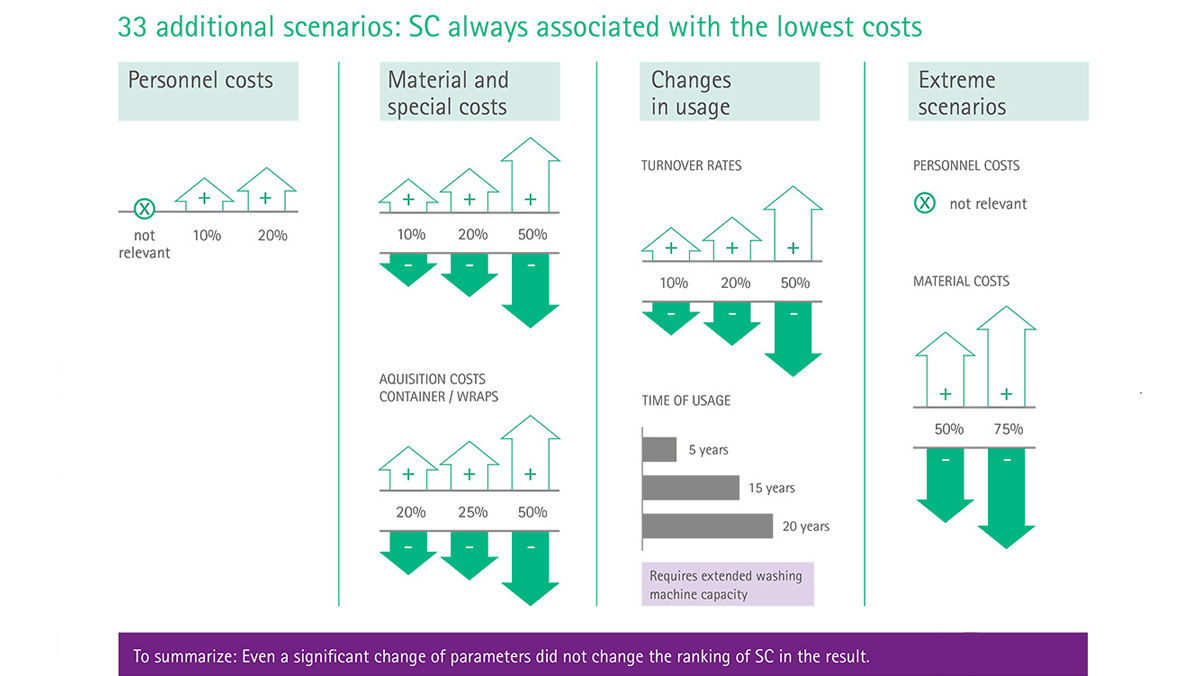

For the acquisition costs of containers and transport baskets, the authors also defined a lifetime – in this case, of ten years – and a turnover rate of 120 units per year.

Consolidating all the information acquired from observations, expert interviews and literature analysis, the authors were able to structure a detailed plan of the 36 sub-processes involved in the wrapping and the 49 sub-processes involved in the container options, and calculated the costs of all four options.

Facts and numbers: what did the authors find?

After the number crunching, the authors determined the following costs for each of the four options.

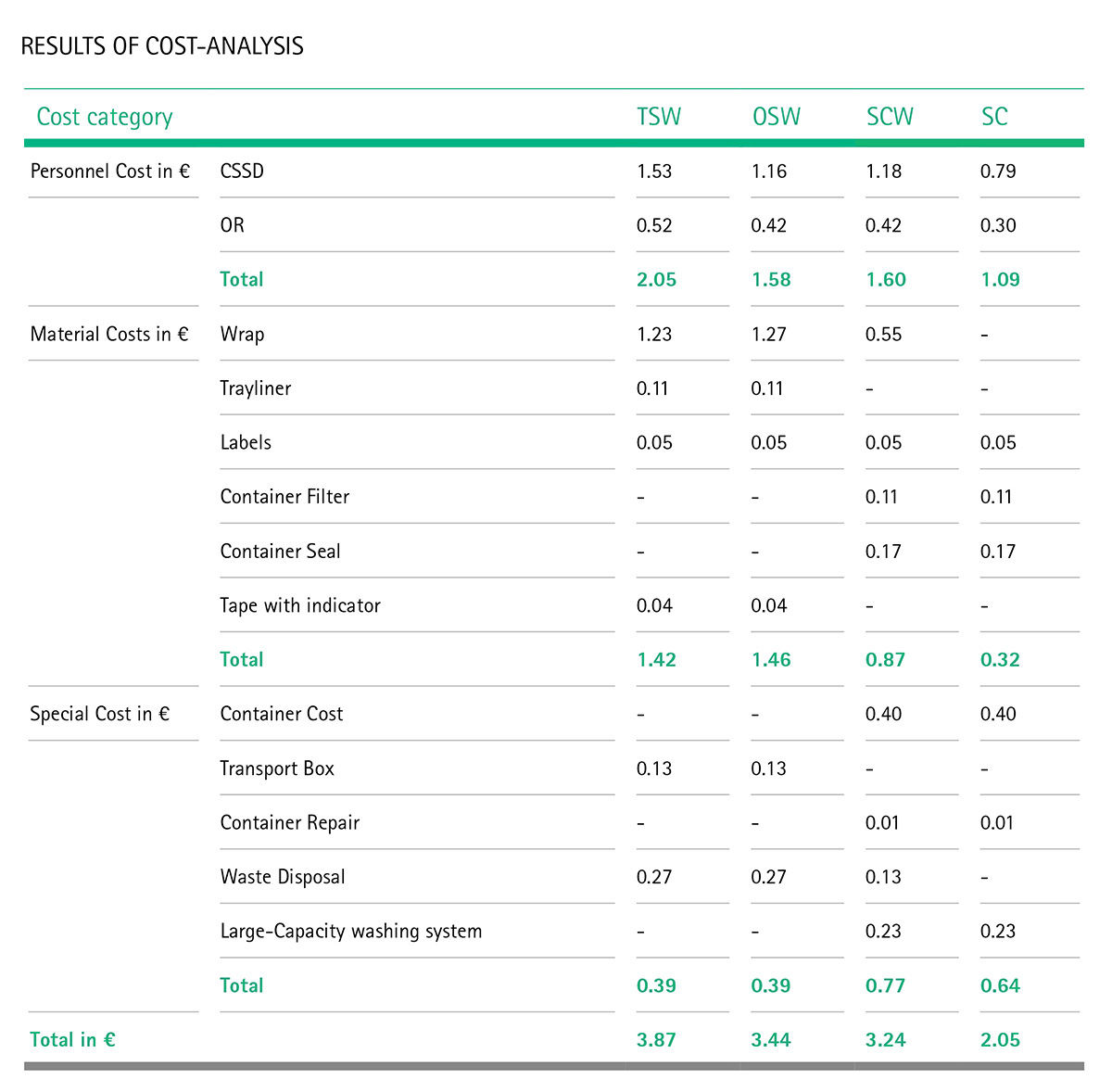

Table 1 [1], [2]

Table 1 [1], [2]